Dr. Madhusudhan Adhikari

Dr. Madhusudhan Adhikari

Nepal stands at a pivotal moment in its energy journey. Long known for its vast hydropower potential, estimated at over 80,000 MW, the country is steadily moving from possibility to production. With hundreds of projects in operation, under construction, or in various licensing and study phases, Nepal is positioning itself not only to meet domestic demand but also to emerge as a significant exporter of clean electricity in South Asia.

In FY 2081/82, Nepal became a net exporter, with imports of 1,681 GWh and exports of 2,380 GWh. “The Urja Marga Chitra 2081,” the latest policy paper on electricity planning, states that by 2035, Nepal plans to produce 28,500 MW, allocating 13,500 MW for domestic consumption and 15,000 MW for export. Yet this transition is far from automatic. The central question is no longer whether Nepal can generate electricity, but whether it can sell it competitively in a rapidly evolving regional energy market.

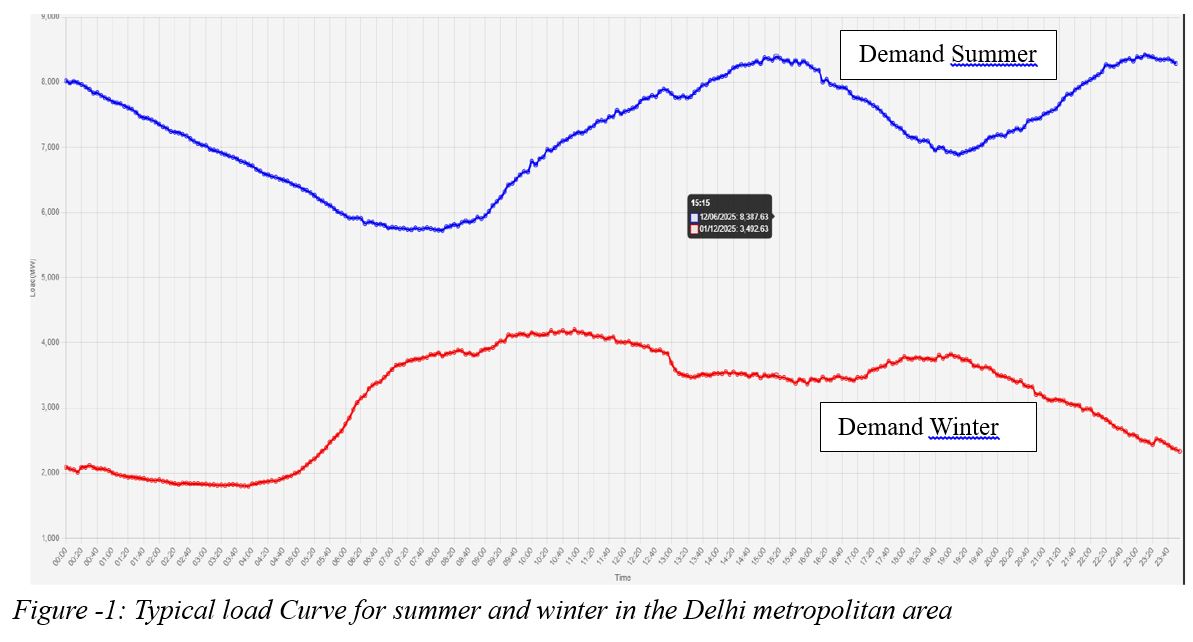

Figure 1 illustrates a typical demand curve of the Delhi metropolitan area, showing that electricity demand in summer is much higher than in winter. As a proxy for the Indian market, this pattern aligns closely with Nepal’s production profile, which is dominated by run-of-river (RoR) projects that generate most electricity during the monsoon season.

This suggests that, all else being equal (“ceteris paribus”), market absorption should not be a major issue for Nepali hydropower. However, the market cannot be viewed in isolation. True demand also depends on non-discriminatory access and price competitiveness.

This suggests that, all else being equal (“ceteris paribus”), market absorption should not be a major issue for Nepali hydropower. However, the market cannot be viewed in isolation. True demand also depends on non-discriminatory access and price competitiveness.

Compared to Nepal, India has already crossed the threshold of 500 GW of installed capacity. This suggests that Nepali electricity is an option rather than a necessity for India, whereas for Nepal, the Indian market is essential.

Expanding Generation – Limited Consumption – Challenging Export

Nepal’s hydropower sector has made notable progress. To date, 208 projects generate around 3,806 MW, a dramatic improvement from the era of chronic load shedding just a decade ago. The future pipeline is even more ambitious: 263 licensed projects (11,098 MW), 62 projects under application (10,699 MW), 189 projects with survey licenses (9,666 MW), and 32 projects in the study phase. In total, Nepal has 729 projects representing over 35,000 MW of potential capacity. This scale far exceeds domestic demand.

As indicated in Urja Marga Chitra 2081 and other demand analyses, the current national peak load remains below 3,000 MW. Future demand growth depends on infrastructure development and consumers’ purchasing power. Under a business-as-usual scenario, GDP and per capita income growth alone will not generate demand sufficient to match electricity generation targets. Although demand will grow with electrification and industrialisation, the gap is so large that electricity export is not optional-it is essential. However, this is only possible if key challenges are addressed, namely: market access, price competitiveness, and transmission infrastructure.

The Export Opportunity and Economic Contradiction

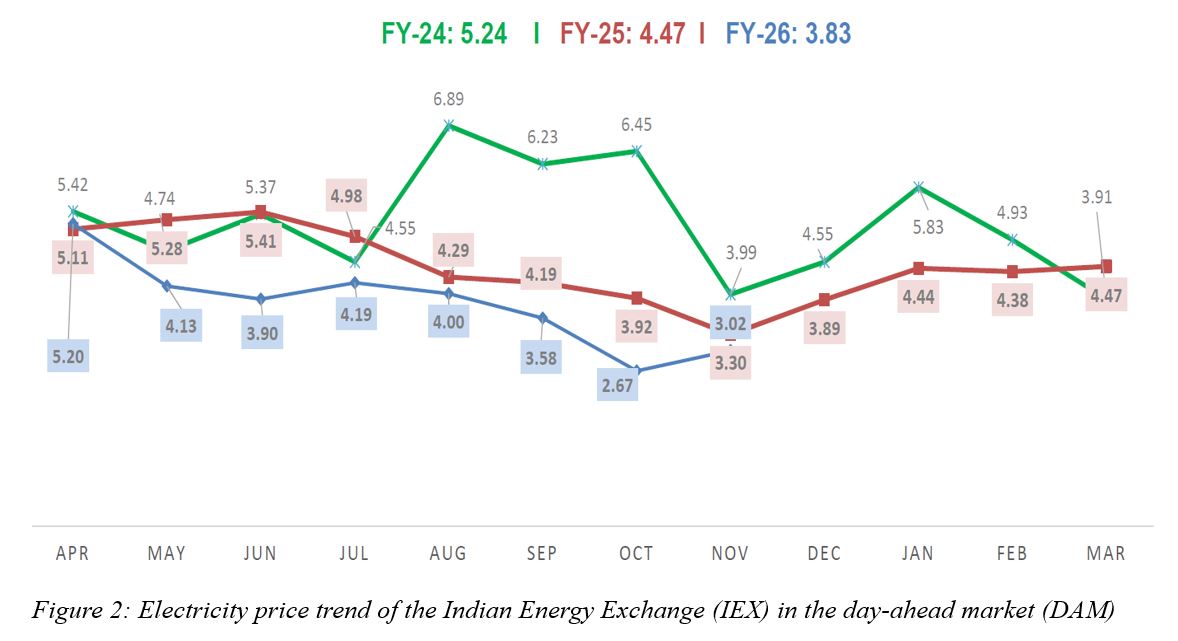

Nepal is well-positioned between two major energy markets, China and India. However, due to proximity to major electricity load centres, grid connectivity, and existing trade arrangements, India remains the most immediate and viable buyer. However, a critical economic contradiction is emerging. The average cost of electricity in Nepal is above NPR 9.00 per kWh, whereas prices in India are typically below NPR 7.00. Figure 2 shows price trends in the Indian Energy Exchange (IEX), ranging from IR 2.67 to IR 5.2 in the current year.

Prices have been declining year-on-year. During peak solar generation periods, prices can even turn negative during daytime hours. This reflects the rapid expansion of renewable energy sources like solar and wind energy in India, creating a structural competitiveness challenge for Nepal. These trends suggest that Nepal is attempting to export relatively expensive hydropower into a market where electricity is becoming increasingly cheaper.

Hydropower offers advantages of firm capacity, storage potential, and grid stability, but these benefits are not always reflected in short-term market prices. Meanwhile, production costs in Nepal are rising due to inflation, bureaucratic delays, land and forest clearance challenges, difficult terrain, climate-related risks, and financing structures.

A central question for Nepal’s electricity trade is “how to improve cost efficiency to compete with Indian market prices”. As a price taker, Nepal must review policies, procedures, implementation modalities, construction practices, and financing mechanisms, effectively applying a reverse-engineering approach to align production costs with market prices.

A central question for Nepal’s electricity trade is “how to improve cost efficiency to compete with Indian market prices”. As a price taker, Nepal must review policies, procedures, implementation modalities, construction practices, and financing mechanisms, effectively applying a reverse-engineering approach to align production costs with market prices.

India’s Strategic Gatekeeping

Beyond pricing, Nepal faces regulatory constraints in accessing the Indian market. The cross-border electricity trade policy of India is governed by a controlled approval system. Export volumes must be pre-approved, and long-term access often requires government-to-government agreements. And then, project-level export eligibility approval depends on ownership structures, including scrutiny of foreign (especially Chinese) investment, construction contracts, and origin of equipment supply. In practice, Nepal cannot freely sell electricity in India; access is conditional, selective, and politically influenced. This creates uncertainty for investors, as project viability depends not only on engineering and finance but also on export approvals and their long-term reliability.

Infrastructure and Seasonal Constraints

Even if market and policy barriers are addressed, physical constraints remain. Transmission infrastructure is a major bottleneck. Domestic evacuation lines lag behind generation capacity, and cross-border transmission capacity is very limited. Despite long-standing discussions, progress has been slow, with only minor initiatives and no breakthrough.

Seasonality adds further complexity. Nepal’s RoR-based system produces most electricity during the monsoon (June–October), dropping to less than 30% of capacity in the dry season. This reduces reliability and weakens Nepal’s position as a dependable supplier. Storage hydropower could address this, but it is significantly more expensive and technically demanding.

Financing Risks and Fragmented Development

Hydropower projects are capital-intensive with long payback periods. While some have achieved financial closure, many remain stalled due to high financing costs, currency risks, and regulatory uncertainty. The large number of projects (729) reflects fragmentation rather than coordinated planning and financing. Developers rely on complex and sometimes inefficient financing mechanisms, increasing cost and risk. Without national prioritisation, such as “a least-cost generation plan”, Nepal risks unstructured overbuilding, leading to inefficiencies and stranded assets.

Priorities for the Strategic Rethinking

Nepal’s approach must shift from supply-driven to market-driven. Key priorities include:

Conclusion: The Point of Policy Shift

Nepal’s electricity sector is at a turning point. It has nearly achieved universal access, a major milestone, but must now focus on quality and reliability. With over 35,000 MW in the pipeline, the challenge is no longer technical feasibility but economic viability and market integration. Falling prices in India, rising costs in Nepal, and policy barriers challenge the narrative of “prosperity through electricity exports.”

Hydropower can remain Nepal’s economic backbone but only if the country shifts from “build and export” to “compete and integrate.” If managed strategically, Nepal can emerge as a regional clean energy leader. If not, it risks building capacity that the market cannot absorb, potentially leading to significant economic and financial consequences for the entire economy.

Dr. Adhikari is a senior energy expert.