Energy Update

Nepal’s Borrowed Resilience: Fuel Dependence and Fragility

-

Ram C. Acharya

Ram C. Acharya

- 20 May, 2026

1. Introduction

Recent turmoil in the oil market has already begun to show up in Nepal in visible ways. Nepali newspapers have reported long queues at fuel stations and pressure on cooking gas supplies. The Nepal Oil Corporation (NOC) has raised petrol and diesel prices repeatedly, citing higher import costs from India, which in turn reflect the wider West Asia shock. India matters enormously here because Nepal depends on it as its fuel supplier. Reuters has also reported that India is facing its worst LPG crunch in decades, with Gulf-linked supply disruptions forcing authorities to cut supplies to industry and scramble for alternatives. Even before shortages become acute, a distant oil shock can quickly turn into local anxiety, higher prices, and fears about basic daily necessities in Nepal.

2. Energy Without Power

This post examines a puzzle at the heart of Nepal’s economy. How can a country that uses so little energy still be so exposed to imported fuel? And how can that same country still look financially comfortable from the outside? The answer lies in a combination of low domestic electrification, high fuel dependence, very large remittance inflows, and unusually strong foreign exchange reserves. Taken together, they create what might be called Nepal’s borrowed resilience. Nepal looks safer than many vulnerable economies, but much of that apparent safety rests on forces beyond its control.

Nepal is often described as an energy-rich country. In one sense that is true. Its rivers descend with force, and its hydropower potential is immense. On paper, that should have made energy one of the foundations of structural transformation, powering industry, transport, irrigation, refrigeration, and rising productivity across the economy. But Nepal’s actual energy story is far more paradoxical. Despite this natural endowment, it remains one of the world’s low-energy economies, and even that low level of energy use is not strongly electrified. That contradiction is not a side issue. It sits close to the center of Nepal’s stalled development story.

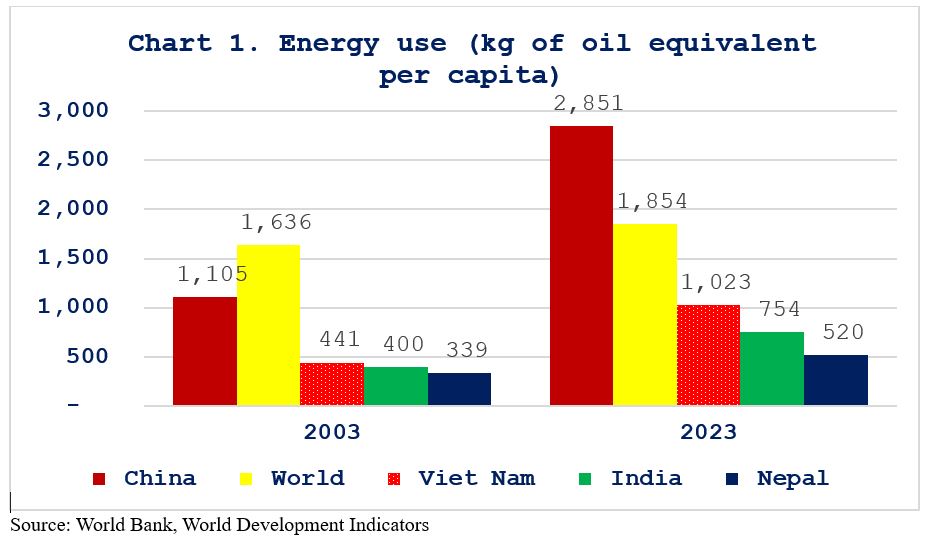

As reported in Chart 1, Nepal’s per capita energy use rose from 339 kilograms of oil equivalent in 2003 to 520 in 2023. That is still well below India, far below China, and less than one-third of the world average. Vietnam is especially revealing in this comparison. It began from a level not dramatically above Nepal’s two decades ago, but then moved upward much faster as development deepened. Nepal’s increase over the period was much slower. This is not a sign of efficiency. It is a sign of low industrial depth, modest mechanization, limited transport intensity, and a still-thin subsistence economy. Nepal uses little energy largely because it still produces too little energy-intensive economic activity.

As reported in Chart 1, Nepal’s per capita energy use rose from 339 kilograms of oil equivalent in 2003 to 520 in 2023. That is still well below India, far below China, and less than one-third of the world average. Vietnam is especially revealing in this comparison. It began from a level not dramatically above Nepal’s two decades ago, but then moved upward much faster as development deepened. Nepal’s increase over the period was much slower. This is not a sign of efficiency. It is a sign of low industrial depth, modest mechanization, limited transport intensity, and a still-thin subsistence economy. Nepal uses little energy largely because it still produces too little energy-intensive economic activity.

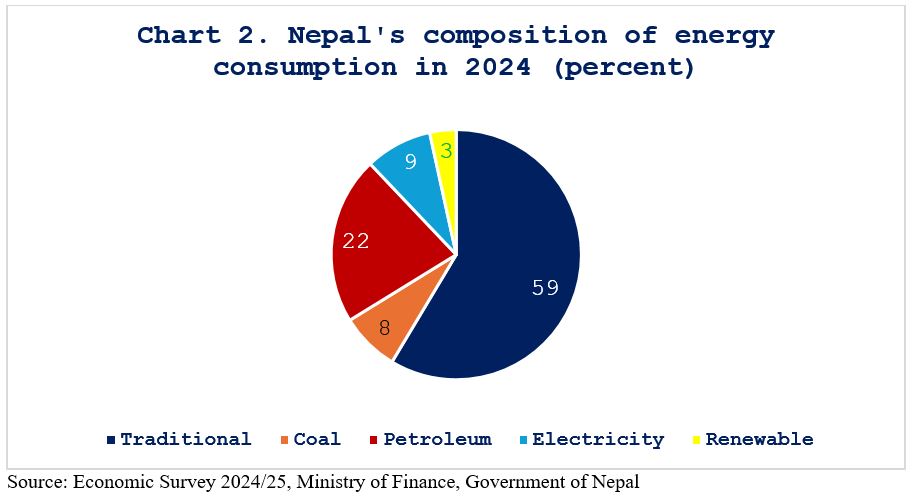

Chart 2 shows why Nepal’s low energy use is even more troubling than it first appears. Traditional biomass (firewood, animal dung and agricultural residues) still accounts for 59 percent of total energy consumption. Petroleum accounts for about 22 percent (which is 54 percent of commercial, that is non-traditional, source). Electricity accounts for only about 9 percent. In other words, Nepal is not only a low-energy economy. It is also a weakly electrified one. Even with abundant hydropower potential, electricity still plays only a small role in total energy use. Much of daily life and economic activity still depends either on traditional biomass or on imported petroleum. That is a poor outcome for a country that speaks so often of energy abundance.

Chart 2 shows why Nepal’s low energy use is even more troubling than it first appears. Traditional biomass (firewood, animal dung and agricultural residues) still accounts for 59 percent of total energy consumption. Petroleum accounts for about 22 percent (which is 54 percent of commercial, that is non-traditional, source). Electricity accounts for only about 9 percent. In other words, Nepal is not only a low-energy economy. It is also a weakly electrified one. Even with abundant hydropower potential, electricity still plays only a small role in total energy use. Much of daily life and economic activity still depends either on traditional biomass or on imported petroleum. That is a poor outcome for a country that speaks so often of energy abundance.

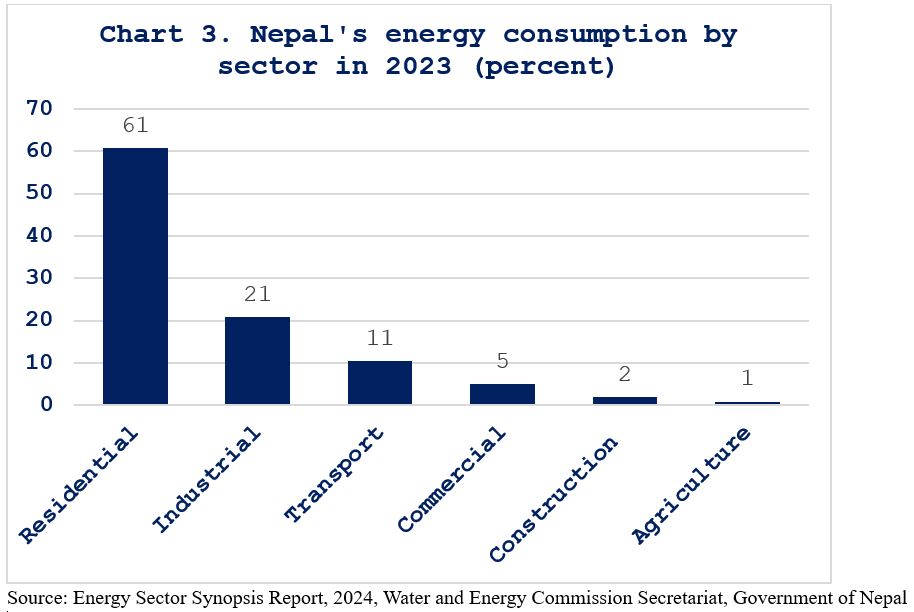

The problem is not only what kind of energy Nepal uses, but where that energy goes. Nepal’s energy structure shows a country still operating in survival mode. Residential use accounts for 61 percent of total energy consumption, but this is not a story of modern household comfort (Chart 3). About 85 percent of that residential energy still comes from traditional biomass. In effect, more than half of all energy used in Nepal is tied to basic household survival through traditional fuels. In Nepal, too little energy goes to industry, transport, and other productivity-enhancing sectors. That helps explain why the country remains so weakly transformed. In a faster-transforming economy, a much larger share would be absorbed by industry, transport, and modern services. In Vietnam, industry accounts for about 50 percent of final energy use and transport 22 percent; in China, 48 percent and 16 percent; in India, 40 percent and 12 percent. Nepal’s pattern is very different. Its energy system is still weighted far more toward sustaining life than powering structural change.

3. The Fuel Trap

3. The Fuel Trap

Low energy use has not made Nepal energy-secure. Despite abundant water resources, and despite decades of hydropower promise, Nepal still depends heavily on imported petroleum for much of its modern energy use. That dependence becomes especially striking when the fuel import bill is measured against the size of the economy.

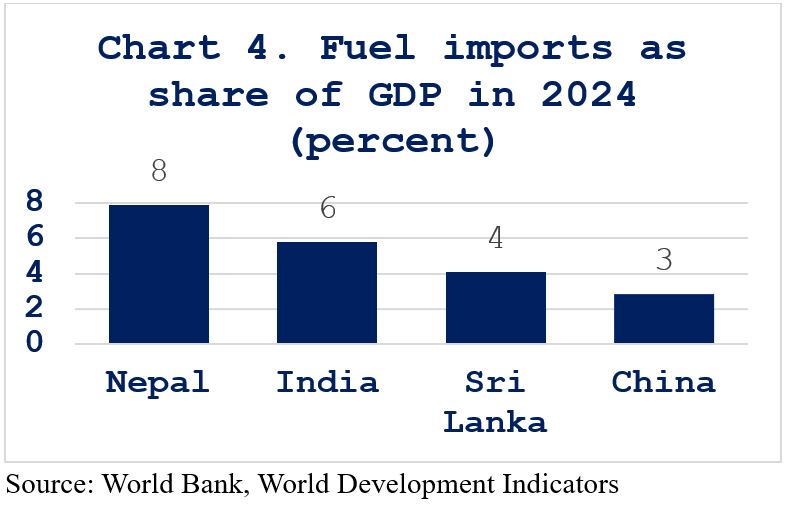

Nepal’s broad fuel imports amount to about 8 percent of GDP (Chart 4). This is the central paradox of the piece. Nepal uses little energy, yet the fuel it does import places a very large burden on the economy relative to its size. India uses much more energy than Nepal, but fuel imports take a smaller share of GDP. China uses vastly more energy, yet its fuel-import burden relative to GDP is far lower. Nepal, by contrast, is carrying a large imported-energy burden without having achieved the industrial or infrastructural gains that often accompany higher energy use. It does not consume much energy, but too much of the energy it does consume still comes from imported fuel.

Nepal’s broad fuel imports amount to about 8 percent of GDP (Chart 4). This is the central paradox of the piece. Nepal uses little energy, yet the fuel it does import places a very large burden on the economy relative to its size. India uses much more energy than Nepal, but fuel imports take a smaller share of GDP. China uses vastly more energy, yet its fuel-import burden relative to GDP is far lower. Nepal, by contrast, is carrying a large imported-energy burden without having achieved the industrial or infrastructural gains that often accompany higher energy use. It does not consume much energy, but too much of the energy it does consume still comes from imported fuel.

This dependence is not merely numerical. It is structural. Nepal buys petroleum through the Indian Oil Corporation channel. That arrangement gives Nepal continuity of supply, and in the current crunch it is fortunate that the agreed system is still functioning. But it also means Nepal’s fuel security depends not only on its own bilateral arrangement with India, but on India’s upstream exposure. About 52 percent of India’s petroleum imports by value come from the Middle East. That also means that about the same percentage of Nepal’s petroleum imports can be ascribed to the Middle East. India has diversified more than Nepal could ever do directly. If India had not diversified, Nepal’s indirect vulnerability would be even greater. Nepal therefore depends on a supply chain that it does not control for a fuel base on which too much of its modern economy still depends.

Nepal’s fuel insecurity is not just a matter of import dependence; it is also a failure of preparation. A decade after pledging to build strategic reserves that could cover around 90 days of demand, the country still appears to have storage capacity for only about 10 to 13 days.

According to Nepal’s Department of Customs, about 55 percent of Nepal’s petroleum imports consist of diesel, 24 percent petrol, and the remaining 21 percent LPG. Diesel and petrol matter across the whole economy: increases in their prices feed into transport costs, food prices, and the cost of almost every activity. This rise in prices will be felt across the economy. But LPG deserves separate attention because it shows more clearly who bears the household side of this external dependence.

Of total LPG consumption, roughly three-quarters goes to the residential sector, with the remaining quarter used in commercial and industrial activities. Nepal household survey data suggest that residential LPG use is concentrated mainly in urban and better-off households. Nationally, 46 percent of households use LPG as their main cooking fuel, whereas 52 percent rely on firewood, and only 0.4 percent use electricity. The urban-rural divide is especially striking. In Kathmandu, 96 percent of households use LPG for cooking; in other urban areas, the figure is about 50 percent; in rural areas, only about 20 percent.

The income gradient is equally sharp. Among the poorest 20 percent of households, only about 13 percent use LPG for cooking, while 85 percent rely on firewood or dung. This means that increases in LPG prices will be borne disproportionately by urban households, especially those in Kathmandu, and more by relatively better-off households than by the poor. By the same logic, any subsidy on LPG is also likely to benefit those groups disproportionately. If the aim of such a subsidy is poverty relief, it would be a poorly targeted instrument.

4. Buffer, Not Strength

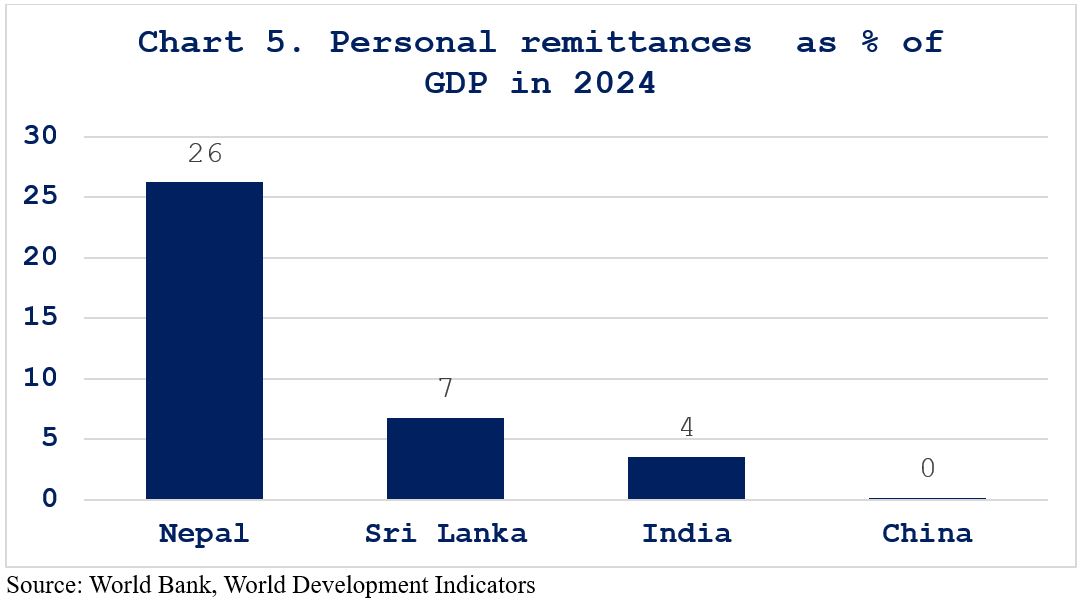

So far, the story has been about dependence on imported fuel. But import dependence is only half the picture. The other half is how Nepal finances that dependence. A country can carry a large fuel bill for some time if it has a reliable source of foreign exchange. In Nepal, that source is overwhelmingly remittances. Remittances reached about 26.2 percent of GDP in 2024 (Chart 5). That is by far the highest figure in the comparison group. It tells us immediately that Nepal’s external position rests heavily on labour earnings from abroad. And the regional pattern matters as much as the total. About 40 percent of those remittances come from the Middle East. That means a flow equivalent to roughly 11 percent of GDP is tied to the same broad region that matters so much for Nepal’s fuel security. This is what makes Nepal’s vulnerability so distinctive. The country is exposed not from one direction, but from two. A shock in the Middle East can raise Nepal’s fuel import bill, while also threatening the labour markets that help finance that bill. Fuel dependence and remittance dependence are not separate stories. They are connected through the same geography of exposure.

And yet Nepal is not entering this period from a position of immediate macroeconomic weakness. The recent oil shock will still be felt nationwide through inflation, disruption, and lower living standards. But Nepal’s position is not the same as that of countries with very weak reserves. As long as supply remains available, Nepal still has the foreign exchange to keep buying fuel. That gives it time, but it does not remove the deeper structural weakness underneath.

And yet Nepal is not entering this period from a position of immediate macroeconomic weakness. The recent oil shock will still be felt nationwide through inflation, disruption, and lower living standards. But Nepal’s position is not the same as that of countries with very weak reserves. As long as supply remains available, Nepal still has the foreign exchange to keep buying fuel. That gives it time, but it does not remove the deeper structural weakness underneath.

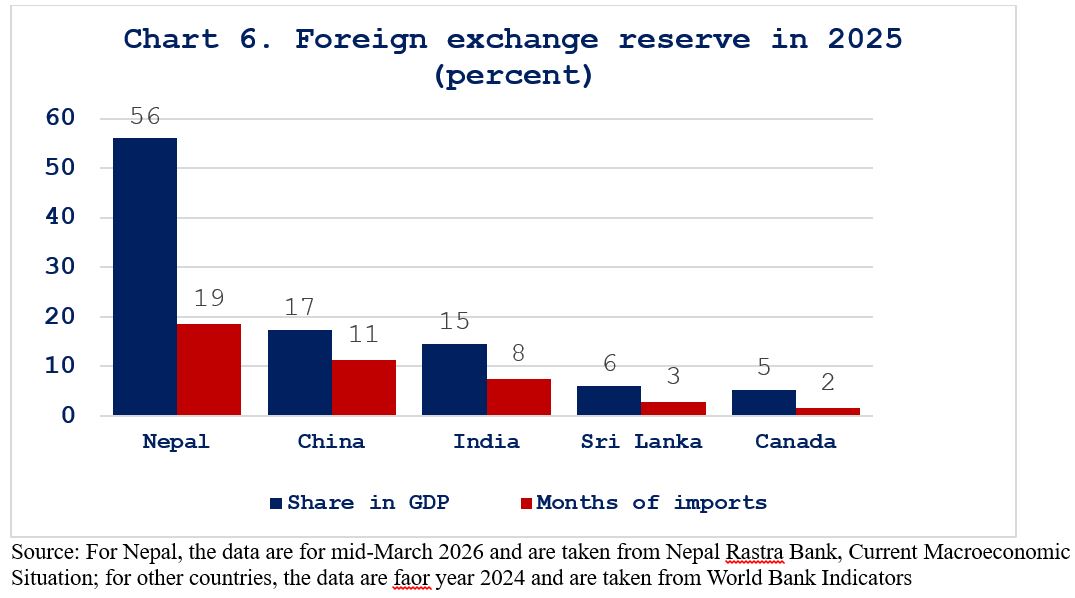

Nepal’s foreign exchange reserves stand at about 56 percent of GDP (Chart 6). Nepal’s foreign exchange reserves in mid-March this year were enough to cover about 19 months of goods and services imports. Those are very large cushions. They place Nepal far above India and Sri Lanka, and at about three times China’s level on these particular measures. In that narrow macroeconomic sense, Nepal is not cornered. It has flexibility. It has room. It has time. This is real, and it should not be dismissed.

However, a country does not become strong simply because its reserve ratio is high, just as it does not become weak simply because its reserve ratio is low. For reference, I have added Canada here. Canada’s reserves are much lower relative to GDP, and those reserves can finance only 2 months of its imports, but that does not make Canada externally fragile in the same way. It simply finances itself through a different kind of economy, one with much deeper domestic production, wider export capabilities, and much stronger institutions of economic adjustment. Nepal’s high reserves therefore should not be read lazily as proof of underlying strength. They are better read as a sign of a particular macroeconomic model, one built heavily on remittance inflows and the foreign exchange accumulation that follows from them.

However, a country does not become strong simply because its reserve ratio is high, just as it does not become weak simply because its reserve ratio is low. For reference, I have added Canada here. Canada’s reserves are much lower relative to GDP, and those reserves can finance only 2 months of its imports, but that does not make Canada externally fragile in the same way. It simply finances itself through a different kind of economy, one with much deeper domestic production, wider export capabilities, and much stronger institutions of economic adjustment. Nepal’s high reserves therefore should not be read lazily as proof of underlying strength. They are better read as a sign of a particular macroeconomic model, one built heavily on remittance inflows and the foreign exchange accumulation that follows from them.

That is why borrowed resilience is the right phrase. Nepal’s resilience is real for this type of oil price rise, but it is borrowed from external earnings rather than fully built at home. Its reserve comfort has not come mainly from a broad export base, strong industrial competitiveness, or a decisive domestic shift toward electrified production and transport. It has come mainly from foreign exchange earned by Nepalis working abroad. That keeps the system functioning. It finances imports, stabilizes the balance of payments, and builds reserves. But it also delays harder questions. A country can sustain itself for quite a long time by exporting people and importing fuel. It cannot call that a durable development model.

The deeper cost is internal. Migration relieves pressure, but it also weakens the pressure to build a more productive economy at home. Imported fuel keeps transport moving, but it masks how slowly Nepal has electrified ordinary economic life despite its hydropower potential. Strong reserves calm markets, but they can also dull urgency in policy. Nepal’s cushion is therefore both a strength and a temptation: it provides breathing room, but it can also encourage complacency.

5. Conclusion

Nepal should therefore be understood as having a strong buffer but a weak structure. The buffer is visible in the reserve numbers. The weak structure is visible in the energy and remittance data. Nepal uses little energy, but too little of that energy comes from electricity. It imports a large amount of fuel relative to GDP despite being a low-energy economy. It depends on the same broad region both for petroleum-linked vulnerability and for a large share of remittance earnings. The country is not as immediately exposed as economies with thin reserves, but its problem is deeper: structural, externally dependent, and not fixable without major policy change.

That is why this moment matters. A distant oil shock has exposed not just Nepal’s vulnerability, but the architecture of its survival. If the conflict deepens, the pressure will not come only through higher fuel costs, but also through risks to the remittance flows on which Nepal depends so heavily. If the country uses this period of reserve comfort to accelerate domestic electrification, strengthen strategic fuel security, and widen its productive and export base, then the current cushion may become a bridge to something stronger. But if we continue on the present path, the reserves will remain what they are now: a valuable buffer, not a solution. They may postpone transformation, as they have in the past, but they cannot substitute for it. That must change.

Email: [email protected]

Blog: https://ramacharya.substack.com

Conversation

More News

- Nepal's First Energy Based News Portal

-

Energy Information Center Pvt. Ltd.

Hemant Marg-11, Babar Mahal, Kathmandu

- Info. Dept. Reg. No. : 254/073/74

- Telephone : +977-1-5321303

- Email : [email protected]